According to the Census Bureau, millennials have overtaken baby boomers as the largest generation in U.S. History. Millennials, or America’s youth born between 1982-2000, now represent more than one quarter of the nation’s population, totaling 83.1 million.

There has been a lot of talk about how, as a generation, millennials have ‘failed to launch’ into adulthood and have delayed moving out of their family’s home. Some experts have even questioned whether or not millennials wantto move out.

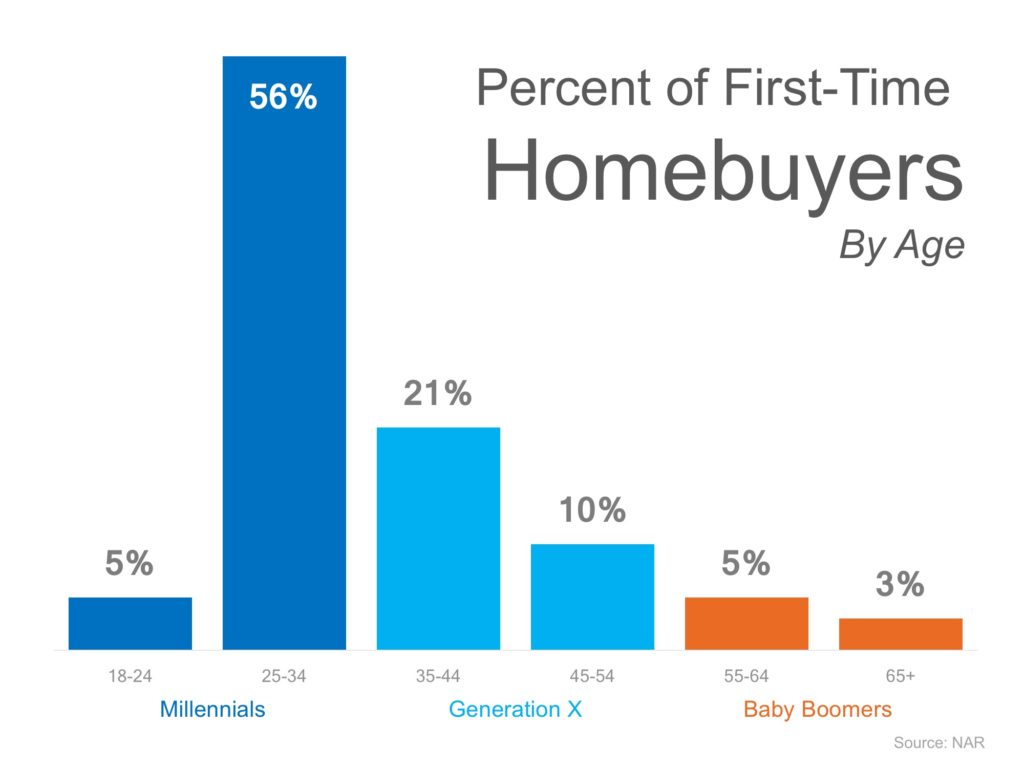

The great news is that not only do millennials want to move out… they aremoving out! The National Association of Realtors (NAR) recently released their 2016 Profile of Home Buyers and Sellers in which they revealed that 61% of all first-time homebuyers were millennials in 2015!

The median age of all first-time buyers in 2015 was 31 years old.

Here is chart showing the breakdown by age:

Many social factors have contributed to millennials waiting to buy their first home. The latest Censusresults show that the median age of Americans at the time of their first marriage has increased significantly over the last 60 years, from 23 for men & 20 for women in 1955, to 29 & 27, respectively, in 2015.

Those who went to college and took out student loans are finally paying them off, as the terms on traditional student loans are 10 years. This means that a large portion of the generation is making its last loan payments and is working toward saving for a first home.

As a whole, the first-time homebuyer share increased to 35% of all buyers, up from 32% in 2014. Not all millennials are first-time buyers, they also made up 12% of all repeat buyers!

Bottom Line

Millennials will continue to drive the housing market next year, as well as in the years to come. As more and more realize that owning a home is within their grasp, they will flock to own their piece of the American Dream. Are you ready to buy your first or even second home?

Are you thinking of buying a home? Are you dreading having to walk through strangers’ houses? Are you concerned about getting the paperwork correct? Hiring a professional real estate agent can take away most of the challenges of buying. A great agent is always worth more than the commission they charge, just like a great doctor or great accountant.

You want to deal with one of the best agents in your marketplace. To do this, you must be able to distinguish an average agent from a great one.

Here are the top 4 demands to make of your real estate agent when buying a home:

1. Tell the Truth About the Price

When making an offer on the home you want to buy, make sure that your agent walks you through their plan for getting both the seller – and the bank – to accept that price. Too many agents will just take the offer that you suggest and then try to ‘work’ both you and the seller in the negotiating phase later. In a competitive market, you need an agent who is going to help you make the best ‘initial offer’ so that you stand out from the crowd. Every house in today’s market must be sold twice – first to you and then to your bank.

The second sale may be more difficult than the first. When prices are surging, it is difficult for appraisers to find adequate, comparable sales (similar houses in the neighborhood that closed recently) to defend the selling price when performing the appraisal for the bank. A red flag should be raised if your agent is not discussing this with you at the time of the original offer.

2. Understand the Timetable with Which Your Family is Dealing

You will be moving your family into a new home. Whether the move revolves around the start of the new school year or a new job, you will be trying to put the move to a plan.

This can be very emotionally draining. Demand from your agent an appreciation for the timetables you are setting. Your agent cannot pick the exact date of your move, but they should exert any influence they can to make it work.

3. Remove as Many of the Challenges as Possible

It is imperative that your agent knows how to handle the challenges that will arise. An agent’s ability to negotiate is critical in this market.

Remember: If you have an agent who was weak negotiating with you on parts of the purchase offer, don’t expect them to turn into a superhero when they are negotiating with the seller for you and your family.

4. Find the Right HOUSE!

There is a reason you are putting yourself and your family through the process of moving.

You are moving on with your life in some way. The reason is important or you wouldn’t be dealing with the headaches and challenges that come along with buying. Do not allow your agent to forget these motivations. Make sure that they don’t worry about your feelings more than they worry about your family; if they discover something needs to be done in order to attain your goal, insist that they have the courage to inform you.

Good agents know how to deliver good news. Great agents know how to deliver tough news. In today’s market, YOU NEED A GREAT AGENT!

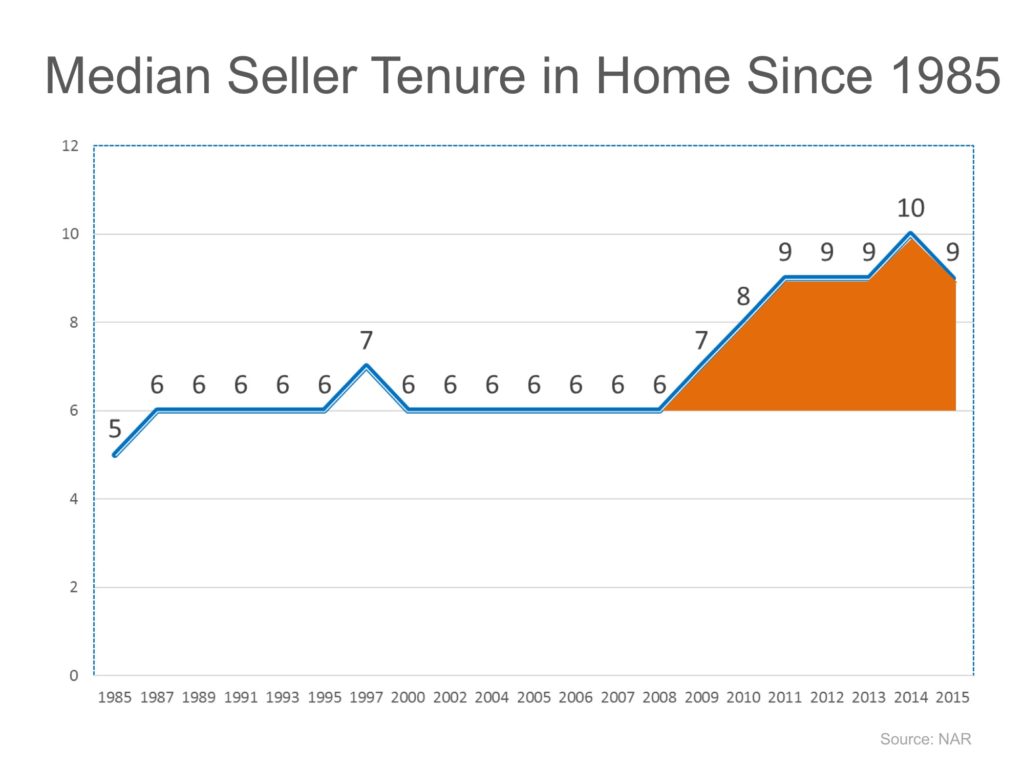

The National Association of Realtors (NAR) keeps historic data on many aspects of homeownership. One of the data points that has changed dramatically is the median tenure of a family in a home. As the graph below shows, for over twenty years (1985-2008), the median tenure averaged exactly six years. However, since 2008, that average is almost nine years – an increase of almost 50%.

Why the dramatic increase?

The reasons for this change are plentiful. The top two reasons are:

The fall in home prices during the housing crisis left many homeowners in a negative equity situation (where their home was worth less than the mortgage on the property).

The uncertainty of the economy made some homeowners much more fiscally conservative about making a move.

However, with home prices rising dramatically over the last several years, over 90% of homes with a mortgage are now in a positive equity situation with 70% of them having at least 20% equity.

And, with the economy coming back and wages starting to increase, many homeowners are in a much better financial situation than they were just a few short years ago.

What does this mean for housing?

Many believe that a large portion of homeowners are not in a house that is best for their current family circumstances. They could be baby boomers living in an empty, four-bedroom colonial, or a millennial couple planning to start a family that currently lives in a one-bedroom condo.

These homeowners are ready to make a move. Since the lack of housing inventory is a major challenge in the current housing market, this could be great news.

The results of the latest Rent vs. Buy Report from Trulia show that homeownership remains cheaper than renting with a traditional 30-year fixed rate mortgage in the 100 largest metro areas in the United States.

The updated numbers actually show that the range is an average of 17.4% less expensive in Honolulu (HI), all the way up to 53.2% less expensive in Miami & West Palm Beach (FL), and 37.7% nationwide!

Other interesting findings in the report include:

Interest rates have remained low, and even though home prices have appreciated around the country, they haven’t greatly outpaced rental appreciation.

Home prices would have to appreciate by a range of over 23% in Honolulu (HI), up to over 45% in Ventura County (CA), to reach the tipping point of renting being less expensive than buying.

Nationally, rates would have to reach 9.1%, a 145% increase over today’s average of 3.7%, for renting to be cheaper than buying. Rates haven’t been that high since January of 1995, according to Freddie Mac.

Bottom Line

Buying a home makes sense socially and financially. If you are one of the many renters out there who would like to evaluate your ability to buy this year, let’s get together to help you find your dream home.

If you are considering selling your home, you may be wondering how your home will really do in relation to the market. Although our market as a whole has been more favorable to sellers in the last few years, demand for an individual property will vary depending on supply of each particular type of home – price point, amenities, challenges, etc.

For example, if a home is in a higher price point, doesn’t have a garage, has a dated kitchen, is on a steep hill, is a far drive into town, etc, the listing may be affected by lesser demand because there may be fewer buyers who can buy that type of property. Everything about a property that causes the potential buyer pool to shrink must be taken into consideration when determining how to price and market a property. Likewise, homes that are expected to have large demand due to popular floorplans and updates have a wider buyer pool and should also be priced and marketed accordingly.

When you are ready to sell, I will review your home from top to bottom, looking for features that provide value for a potential homebuyer. A finished basement? That increases the value. Spare space in the garage? That will also increase the value.

I will also look for things that will shrink the buyer pool which will cause a home’s value to decrease. Deferred maintenance, older systems such as an older water heater or furnace, awkward floorplans, a lot of stairs, older roof or even a strange color palette may be more than some buyers want to deal with and therefore, the market price will need to reflect the lesser demand unless these are things that are going to be corrected before a home goes on the market.

It is also important to look at current buyer trends to determine features that might increase or decrease demand for the home. For example, large lawns are starting to go out of favor with certain buyers who want less maintenance and to reduce water consumption, but just a few years ago, they were all the rage. Demand for large home offices and big entertainment centers is also waning with our changes in technology. Have an updated master suite with a steam shower and updated shower heads or smart home technology? These are currently in high demand and the market price should reflect that positively.

Additionally, the new generation of homebuyers (Millennials) have different needs in their homes than previous generations so we can continue to see buyer demand shift in the coming years.

Want to know more about market demand for your particular type and style of home? Just give me a call at (253) 222-2626 or send an email to john@altitude-re.com. I’ll show you how I determine the market value of your home based on supply and demand.

The US Department of Agriculture is making some changes to its Single Family Housing Guaranteed Loan Program (also known as a USDA loan) effective October 16, 2016. These changes can mean big benefits for anyone considering a home purchase in a rural area in the coming year.

A USDA mortgage allows for a minimal cost of entry in order to make homeownership affordable and attractive in rural areas. However, many areas just outside of urban areas can qualify for a USDA loan. According to TheMortgageReports.com, geographically-speaking, about 97% of the US is eligible for a USDA loan. There are caps on the total value of the home as well as household income limits. Both of these caps will vary by area. In general, a minimum credit score of 640 is required.

The USDA loan provides a loan up to 100% of the home value with an upfront loan guarantee fee and an annual guarantee fee (which is paid monthly). That means that no down payment is required for a USDA loan, a barrier for many would-be homeowners. However, there is a fee for this convenience: both a one-time, upfront fee and an annual fee (reflected as monthly mortgage insurance):

Up Front Lending Fee – this is dropping from 2.75% to 1.0%. On a $300,000 loan, this would now add $3,000 to the loan amount (down from $8,250).

Annual Fee – The annual fee, paid monthly, will be .35% of the average scheduled unpaid principal balance, down from .5% this last year. For an unpaid average balance of $250,000, the amount saved per month will be a bit more than $30 under the new parameters.

These fees are actually less than an FHA-backed loan (which require 3.5% down payment) which also requires an Up Front Lending Fee (of 1.75%) and an Annual Premium which is also paid monthly. The Annual Premium for a 30 year loan with 5% down payment (or equity) or less is .85% (based on initial loan-to-value ratio).

Both 15 year and 30 year fixed rate mortgages are available with a USDA loan and the funds can only be used for primary residences.

One thing to note is that the lender may have additional fees to be aware of such as origination fees, fee to pull a credit report, etc. Additionally, there are other closing costs that you will need to budget for as per your lender.

There are a lot of financial benefits to a USDA loan and those benefits are getting better. If you would like to learn more, please contact me at (253) 222-2626 or email john@altitude-re.com. I can put you in touch with a lender who can discuss all the ins and outs of this program with you and help you determine if this program meets your needs.

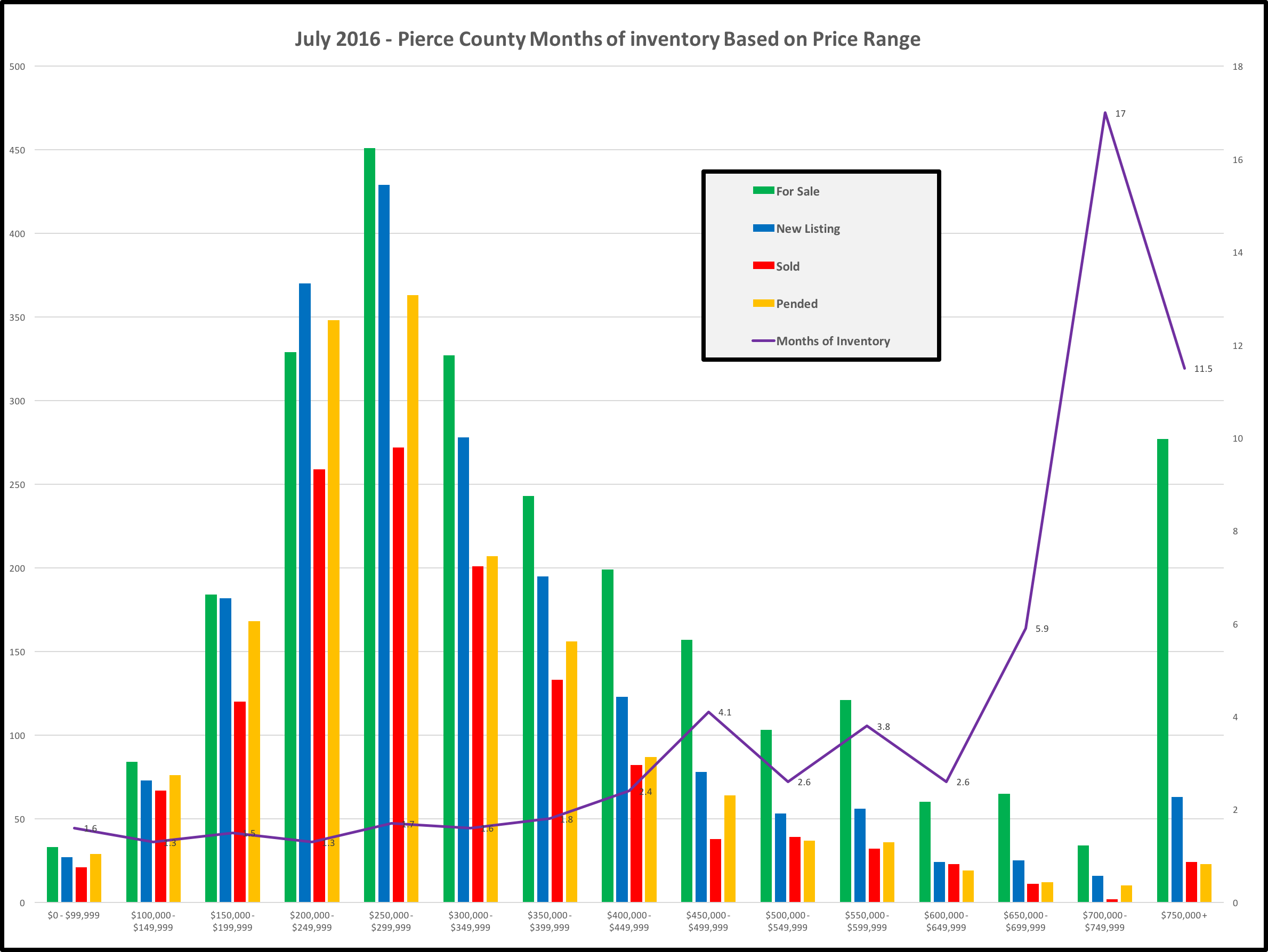

I consider myself a geek. I love geeking out over numbers and in Real Estate there is no shortage of numbers to geek out over. For those of you that have read or watched my market updates in the past, you know that one of the indicators I like to watch is “Months of Inventory”. This can help you figure out if you’re in a balanced market, a seller’s market or a buyer’s market. In general, 0-3 months worth of inventory is a Seller’s market, 3-6 months of inventory is a balanced market and anything over 6 months worth of inventory is a buyer’s market. Many of you will remember our buyers market was defined as 2008 – 2011.

Real Estate is cyclical. After having done this now for close to 14 years, I’ve seen the cycle. I’m working on my second one. I watched as the market ran up 2003 – 2006 . . . fell 2007 – 2011 and have been watching it rise since 2012. Change IS in the air my friends. No one can accurately predict when that change will come, but it will come. Some people think it’s already starting, and in some areas of the country, they may be right. Some people think it’s a year or two away. Regardless the change will come.

The other thing Real Estate is, is local. I have a client who’s home was on the market for 30 days before she received an offer. She was stressing and calling me nearly every day saying “When are we going to get an offer?” and “My neighbor’s home sold in 6 hours” and “My friends told me their neighbor’s home sold in a day”. Of course no one is saying “My home took 3 months to sell” or “I tried selling and couldn’t”, but those two scenarios are just as likely and the others. NEWSFLASH: Every house doesn’t sell. Every house doesn’t sell in 1 hour or even 1 day or heaven forbid, even 1 week. In the case of my client, average market time for homes in her area in her price range was 28 days. We got an offer on day 31.

When I say that Real Estate is local, I mean it’s local. Your neighborhood, is different than the next neighborhood over. Your home even though it might be the “same” as your neighbor’s is different. When you say “They got an offer in 6 hours” what were “They” selling? Right now in Pierce County, if you have anything relatively nice under $250,000 you can probably expect it to sell fairly quickly. If “Their” home was a 3 bedroom 2 bath home for $235,000, priced well, staged well in a desirable community and school district, it probably DID sell in 6 hours. But you can’t compare that to a home that’s listed for sale at $450,000. They are two different animals. The pool of buyers for a $450,000 home is smaller than the pool of buyers for a $235,000 home. It’s just a fact of economics.

So what I did was put together this handy chart showing you what inventory levels are like in different price ranges for ALL of Pierce County. Again, Real Estate is local. So if you happen to have a $235,000 home in Pierce County, that doesn’t mean that where your home is has exactly 1.3 months worth of inventory. Elbe for example will have more months of inventory than University Place. People are lining up to buy homes in University Place, people pass THROUGH Elbe on the way to Mount Rainier. (Sorry to both of you that live in Elbe and are reading this) Real Estate is Local. Real Estate is Cyclical. If you want specific information for YOUR home, let me know and I’m happy to put together a personalized report just for YOU.

Notice that as you get above $400,000 in Pierce county, inventory starts to rise. As a side note, I did this same analysis in King County and not until you get above $1,250,000 do you have more than 2 months worth of inventory. Crazy town. It’s a Seller’s market in every price category up through $1,500,000 . . . which is where I stopped because I didn’t want to make myself throw up.

Have a look, comment below! Click on the image for a larger version…

Months of Inventory by Price Range in Pierce County, Washington

Preparing Your Home for Fall

I cannot believe that fall is upon us! Although we have had a wonderful summer, it is time to begin planning for fall maintenance on your home. The changes in the seasons can be tough for home structures, so to prevent surprises when your home is at its most vulnerable, take a day before autumn takes hold and prepare your home for the months ahead. Roof and siding

The baking heat of summer can cause materials on your roof and siding to shrink and expand, leaving gaps. Although the solution to remedy these gaps may vary depending on the type of materials your roof and siding consists of, take note of any gaps you see between joints (at seams, between siding and window/door openings, at transitions from wall to roof, etc) or between roofing materials (around skylights, between shingles or tiles, around flashing, etc). These may be easy fixes or it may be time to call in a professional. Keeping water and bugs out and keeping heat in is the name of the game! Gutters

While you or your roofer are up on the roof, take the time to check your gutters both for debris (which needs to be cleaned out) and structural integrity. Gutters that are in disrepair may not be able to channel water away from your roof and house, so making sure these are in good working order is imperative. Weather Stripping

Weather stripping around doors also should be looked at in the fall. This is an inexpensive do-it-yourself chore that most people can tackle. Again, you want to keep toasty air in and pests out, so making sure your stripping isn’t too old to be up to the task is a must. Chimney

Before you begin any fires, have your chimney inspected. According to the Chimney Safety Institute of America, a clean chimney not only helps prevent chimney fires, it also allows flue gases and smoke to travel freely up and out of your home. Chimneys should be inspected annually and clean and repair what is necessary. Service Furnace

As we are winding down from summer, doing our fair share of sweltering, it may be difficult to think of your actually needing to turn on the heater, but preventative maintenance now is a lot cheaper than an emergency call on a frigid Friday night.

Maintaining your home and preparing it for the fall and winter months not only makes sense from a comfort point of view, it also can save you money in terms of utility costs and can keep the value up when it is time to sell. Please give me a call, text, or email to learn more: (253) 222-2626 or john@altitude-re.com.

Housing Starts

With our population on the rise and housing demand high across the country, you might be wondering why builders just don’t build more homes to satiate the demand. According to the New York Times, the United States added 1.24 million households per year on average between 2000 and 2007. Then add in the average 300,000 homes that need to be repaired or replaced and we get about 1.5 million new households needed per year to keep up with demand (both single family and multifamily). However, during the economic downturn, many builders could not build and some even got out of the business. We have been behind in terms of demand for several years now, which is why many areas are seeing such high demand for housing, multiple offers, and notable increases in the median sales prices.

According to Census data compiled by the National Association of Home Builders, the U.S. is currently (as of June 2016) at an annual adjusted rate of 1,189,000 starts – well below the needed 1.5 million needed for the year. The chart below shows monthly housing starts since 1959. The average from 1959-2015 has been 1,441,000 units.We have a ways to go to catch up, but builder confidence is strong and housing starts should rise as confidence increases. Want to know more about what this means for our area? Give me a call, text, or email (253) 222-2626 or john@altitude-re.com.

Preparing for Multiple Offers – The Pros and Cons of an Offer Review Date

Buyers are out and demand for homes is high! When it is time to list your property and if multiple offers are expected, there will be a number of issues and strategy for us to consider. One of the primary issues is whether or not to have an offer review date, or a date in which any offers from buyers are due. In theory, this allows all offers to have a fair shot as they would be presented at the same time. However, there are pros and cons to this practice and there are still buyers who may try and circumvent the competition. The pros of an offer review date: In addition to indicating to the public that demand is expected to be high and therefore piquing interest, this also encourages buyers to act with haste. In addition, this generally encourages serious buyers to make serious offers. The cons of an offer review date: In the event the property doesn’t get offers and need to retract the offer review date statement in the MLS, this may make the listing look less appealing or make buyers wonder why no offers were made.

If you do choose to have an offer review date, we will discuss a week to ten day strategy that includes a brokers open if possible (an open house for real estate agents), a public open house (if your home is in an area with successful open houses), and enough time for buyers to do their due diligence and learn what they need about the property before making an offer.

I will be gathering the offers and specifics at the deadline and will present them to you in a way where you can easily analyze the pros and cons of each. You will have an opportunity to negotiate with the buyers as well.

If you decide that an offer review date is a strategy you would like to employ, one thing we will discuss is what happens when a buyer decides to make a strong offer right out the gate that expires before the offer review date. This is a strategy that some buyers make, appealing to sellers’ desire to have an offer accepted and proceeding to close in order to avoid competing with other buyers (the bird in the hand is worth two in the bush philosophy). Of course, there are pros and cons to accepting an early offer; the offer may be lower or not as strong as the offers that come in at the offer review date and in the event that this offer doesn’t close, there may not be a backup offer in place. However, if the seller waits for additional offers to come in, there may be none forthcoming.

There are a lot of options here, but when it is time to list your home, if we expect multiple offers, I will review all your options with you, present all the pros and cons of each option, but you will ultimately be in the driver’s seat. Questions? Let’s talk! Give me a call, text, or email: john@altitude-re.com or (253) 222-2626.

Buyers are out and demand for homes is high! When it is time to list your property and if multiple offers are expected, there will be a number of issues and strategy for us to consider. One of the primary issues is whether or not to have an offer review date, or a date in which any offers from buyers are due. In theory, this allows all offers to have a fair shot as they would be presented at the same time. However, there are pros and cons to this practice and there are still buyers who may try and circumvent the competition.

Buyers are out and demand for homes is high! When it is time to list your property and if multiple offers are expected, there will be a number of issues and strategy for us to consider. One of the primary issues is whether or not to have an offer review date, or a date in which any offers from buyers are due. In theory, this allows all offers to have a fair shot as they would be presented at the same time. However, there are pros and cons to this practice and there are still buyers who may try and circumvent the competition.